News

Insight is power

Energy Market Update for March 2016

Our latest energy update providing insight into market trends

for gas, power & oil, and what to watch throughout the month.

Market Summary

Gas – During March, gas decreased slightly along with a slight increase between 15th-18th.

Power – Power offers have increased by £1.75 /mwh since the start of March.

Oil – Despite a brief slowdown mid-month, we have seen a sustained growth in prices.

Direction of Market Price (Annual Comparison)

After what was a terrible start to 2016 on the equities market, March saw a sustained rebound where the FTSE 100 climbed above 6,000 and eventually pushed its way to 6,200. Fears about the Brexit and reaction to the Budget did little to dampen what has been an interesting month for Markets.

Gas

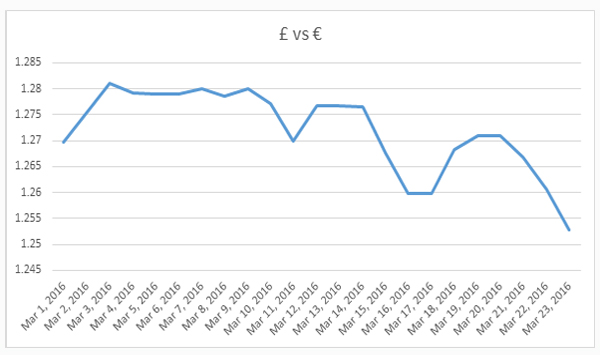

Despite the increase in Oil prices, Gas prices overall have decreased slightly. Generally the UK system has been oversupplied due to slightly lower demand than seasonal norms, there was a one week exception where demand rose from 255 mm cm to around 300 mm cm; this spike in prices can be seen from 15/03 – 18/03 on the graph below. Another interesting development throughout March has been the volatility of the British Pound, which we can directly link to the daily volatility in the Gas Market.

Power

This volatility of the British Pound has had an adverse effect on the Power Market, more so than the Gas. This has resulted in some Power Curves being pulled, most notably GDF. Power offers have increased by £1.75 /mwh since the start of March, with a large spike recently – due to events in Brussels. The political implications of recent events are destined to have some effect on Currencies Markets but it has yet to be seen what direction the pound will take. Significantly, Demand is average for this time of year, however with the clocks going forward at the end of this week demand is due to decrease.

Oil

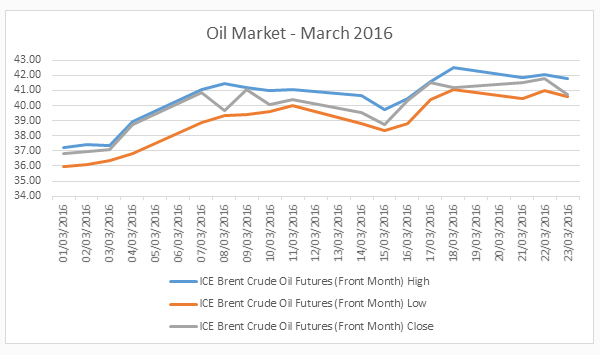

If we look at the Oil Market, despite a brief slowdown mid-month we have seen a sustained growth in prices, where finally the markets broke the $40 /bl threshold, in what is a very cautious market breaking that $40 /bl marker was huge. Interestingly, when we look deeper, fundamentals have not changed, there is increasing doubt over the state of the Chinese Economy and the Eurozone Economy, the US releases reports where one week prompts markets to rejoice and another week markets to ponder to worst and in addition to a US Presidential Race to contend with. The most notable influence on the Oil Market has been the move to bring out a ‘Production Freeze’ within Oil Producing Countries this production freeze would help to stop the continued oversupply of Oil into the Market. What is interesting is the fluctuations throughout a day’s trading, during February there were some violent swings, however trading throughout March was much calmer.

What to watch out for throughout April:

April will most certainly revolve around the potential meeting between OPEC nations during the middle of the Month, if Saudi Arabia and others can convince Iran to cut their production we could see Oil Prices break the $45 /bl thresehold or even $50 /bl. This will then filter through the Gas and Power Offers. Also, we must keep a close eye on Political and Economic announcements that in the coming months may change the landscape of not only the UK, but the Eurozone and the USA.

Topics of Interest: